UiPath が上場するので Form S-1 をさらっと読む

有名な RPA のユニコーン1 である UiPath が上場するらしい。

https://jp.techcrunch.com/2021/03/29/2021-03-26-a-first-look-at-uipaths-ipo-filing/

自分は UiPath を使ったことがない(Zapier はよく使う)のだが、せっかくなので Form S-1 を軽く読んでみた。

https://www.sec.gov/Archives/edgar/data/1734722/000119312521094920/d98556ds1.htm

主要な指標

2021 年 1 月期の主要な指標は以下の通り。

ARR (Annualized Renewal Run-Rate または Annual Reccurring Revenue の略)は毎年繰り越される収益のことで、一般的には以下を意味する。

ARR = 前年の収益 + 新規契約やアップグレードで得る収益 - 解約やダウングレードで失う収益新規顧客を獲得しつつ既存顧客との関係を維持・拡大する能力を示す指標なので、収益の積み上げが重要になる SaaS 企業の開示でよく使われる。

UiPath における ARR の定義は Form S-1 の 75 ページに書いてある(実は同じ ARR という用語を使っていても各社定義が異なるので単純比較は難しい)。クソ長いので一部だけ引用すると

We define ARR as annualized invoiced amounts per solution sku from subscription licenses and maintenance obligations assuming no increases or reductions in their subscriptions. ARR does not include the costs we may incur to obtain such subscription licenses or provide such maintenance, and does not reflect any actual or anticipated reductions in invoiced value due to contract non-renewals or service cancellations other than for specific bad debt or disputed amounts.

とのことなので、 UiPath のライセンスと保守契約による売上を含み、将来の解約予定を含まないようだ。

Customers >= $100k ARR

UiPath を見てまず最初に気になったのは、 Customers >= $100k ARR つまり年間 10 万ドル以上を支払う顧客が 1,002 社いて全体の約 13 % を占めていることだった。米国で上場している企業向けソフトウェア開発企業はこの指標をよく出している。

開示する理由は会社によるだろうが、この指標が安定して成長することは

- 大きな企業の課題を解決できている

- Paid Customer が成長に従って他のサービスに乗り換えない

ことを意味している。

昔 Slack が上場したときに同じ指標を出していた(昔書いたブログ)のだが、 Slack は 2019 年 1 月期で Paid Customer 88,000 に対し $100k/year 以上の支払いを行う顧客は 575 で、これは全体の 1% にも満たない。この指標は企業間で比較するというよりは「同じ会社の」時系列で比較して評価する(安定して伸びていれば OK)のが正しい使い方だと思うが、この 13% という数字はかなり高いのではないか。

実際に、 UiPath は大企業から多くの収益を得ている。 78 ページを読むと、

For example, as of January 31, 2019, we had 305 customers with ARR of $100,000 or more and 21 customers with ARR of $1.0 million or more, which accounted for 69% and 27% of our revenue, respectively, for the fiscal year then ended. As of January 31, 2020, we had 597 customers with ARR of $100,000 or more and 43 customers with ARR of $1.0 million or more, which accounted for 69% and 25% of our revenue, respectively, for the fiscal year then ended. As of January 31, 2021, we had 1,002 customers with ARR of $100,000 or more and 89 customers with ARR of $1.0 million or more, which accounted for 75% and 35% of our revenue, respectively, for the fiscal year then ended.

とのことなので、2020 年 1 月期は売上の 69%、2021 年 1 月期は実に 75% が $100k 以上の ARR の顧客から生じている。なお、 78 ページの記載によれば Fortune 10 の 80% と Fortune Global 500 の 63% が UiPath の顧客であるとのことだ。

Dollar-based Net Retention Rate

これは新規契約を含まない、既存顧客のみからの売上の伸びを示す指標としてよく使われる。 78 ページを読むと、

Further evidence of our land-and-expand business model is our dollar-based net retention rate, which was 153% and 145% as of January 31, 2020 and 2021, respectively. We calculate dollar-based net retention rate as of a period end by starting with the ARR from the cohort of all customers as of 12 months prior to such period-end, or the Prior Period ARR. We then calculate the ARR from these same customers as of the current period-end, or the Current Period ARR. Current Period ARR includes any expansion and is net of contraction or attrition over the last 12 months, but does not include ARR from new customers in the current period. We then divide the total Current Period ARR by the total Prior Period ARR to arrive at the point-in-time dollar-based net retention rate.

とのことなので、既存顧客からの売上が FY2019 → 2020 と FY2020 → 2021 でそれぞれ約 1.5 倍ずつ増えていることが分かる。

また、同じページによると解約によらない ARR の割合が 96 ~ 97% とのことなので、ほとんど全ての顧客は満足して UiPath を使っているようだ。

Furthermore, our dollar-based gross retention rate, which is the percentage of ARR from all subscription customers as of the year prior that is not lost to customer churn, was 96% and 97% as of January 31, 2020 and 2021, respectively. We calculate our dollar-based gross retention rate as of a period end by starting with the ARR from the cohort of all subscription customers as of 12 months prior to such period-end, or the Prior Period ARR. We then deduct from the Prior Period ARR any ARR from subscription customers who are no longer customers as of the current period end, or the Current Period Remaining ARR. We then divide the total Current Period Remaining ARR by the total Prior Period ARR to arrive at the point-in-time dollar-based gross retention rate. Because our dollar-based gross retention rate reflects only customer losses and does not reflect customer expansion or contraction, it demonstrates that the vast majority of our customers continue to use our platform and renew their licensed software.

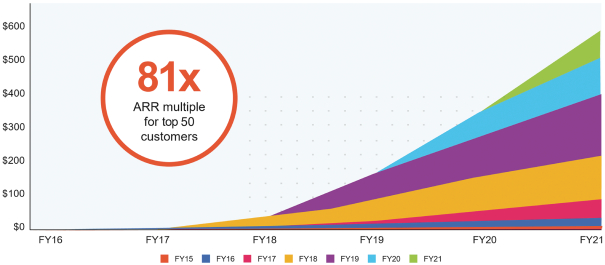

既存顧客からの売上の伸び

UiPath は初回導入後、サポートを通じて顧客の engagement を高めることで収益を伸ばしている。 77 ページの記載によると

For example, the 2016 cohort includes all customers that had their initial purchase within the fiscal year 2016. This cohort increased their ARR from $395,368 as of January 31, 2016 to $22.7 million as of January 31, 2021, representing a multiple of approximately 57x since fiscal year 2016.

とのことで、2016 年 1 月期に使い始めた顧客の ARR は 5 年後の 2021 年 1 月期には約 57 倍となっている。

また、2021 年 1 月期の売上上位 50 社からの売上は(その顧客の初月時点での契約から計算した仮想的な ARR と比べて)中央値で約 81 倍に伸びているそうだ。

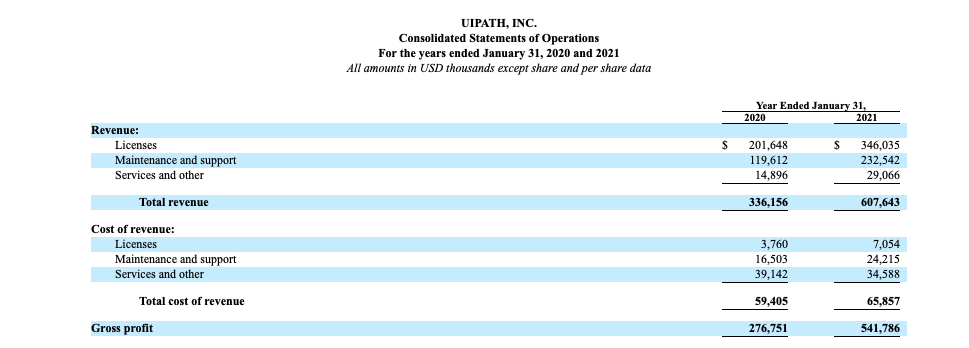

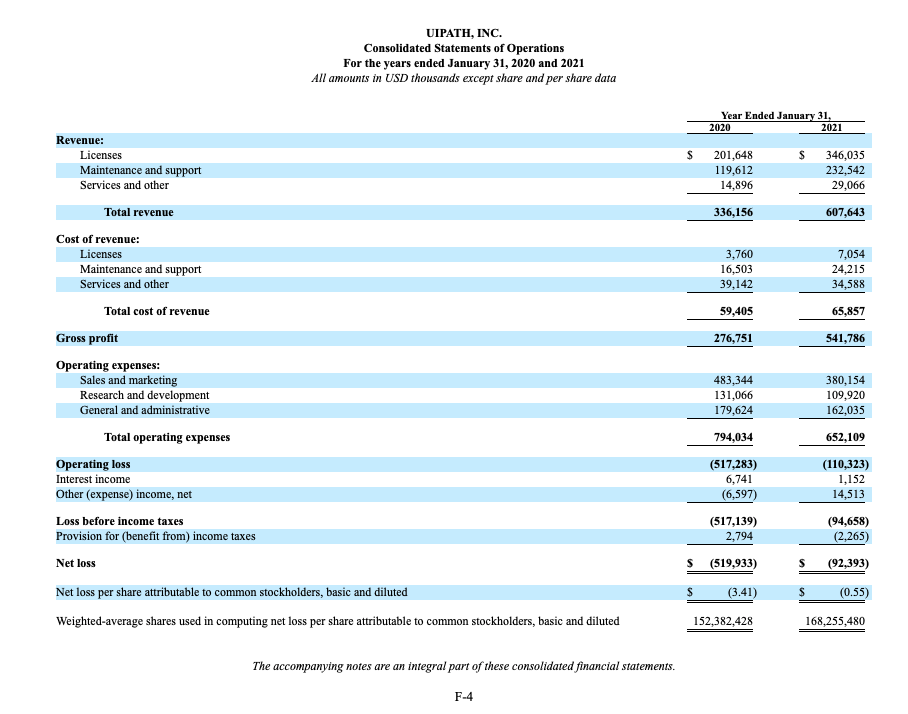

売上の内訳

UiPath の売上の大部分は License と Maintainance and Support で構成されている。

2021 年 1 月期決算では License による売上が $346,035k (売上の 57%)で Maintainance and Support が $232,542k(売上の 38%)だった。その前年は License が $201,648k (売上の 60%)で Maintainance and Support が $119,612k(売上の 36%)だ。

このそれぞれが具体的に何を指しているのかは Revenue Recognition の箇所を読むと書いてある。

Revenue Recognition

自分が US の会社の開示を読むときはまず Revenue Recognition で検索してそれを読むようにしている。 UiPath の Form S-1 でいうと 94 ページのあたり。

これの何がいいかと言うと、その会社が得る収益の内容や収益獲得のプロセス、適用される会計基準が 1 ~ 2 ページで簡潔に記載されていることにある。英語を何百ページも読むのは疲れるので、必要な箇所だけ読みたい。

ここを読むと License は文字通り UiPath のソフトウェア・ライセンスで、期間限定のものと無制限の永久ライセンスがあり、顧客がそのソフトウェアを使用して便益を獲得できる状態になった(ライセンス対象期間が開始した)時点で収益を認識している、と書いてある。

Maintainance and Support は期間限定ライセンスと永久ライセンスの双方について技術サポート(stand-ready 型の契約で、提供期間に応じて認識される)やアップグレードを提供した売上とある。

売上の残り 5% 程度を占める Services and Other は顧客へのトレーニングサービスの提供等を含んでいるらしい。

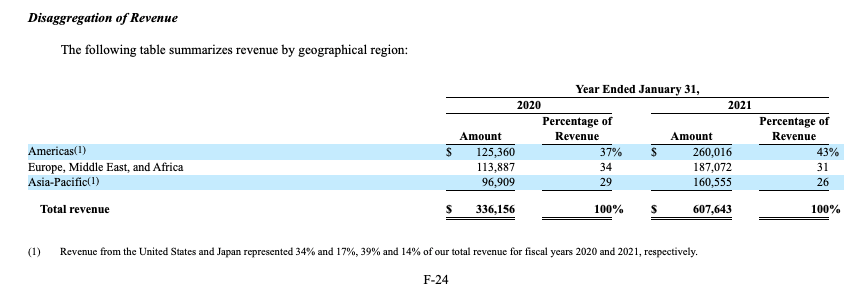

地域別の売上

全地域で売上が大きく伸びているが、全体に占める割合は南北アメリカが 43% で最も多い。

下に小さく書いてあるが日本での売上が FY2020 で全体の 17%、 FY2021 で全体の 14% あるらしい。それぞれ売上にかけると、金額としては FY2020 で $57M、 FY2021 で $85M になる。ちなみに $85M は規模感でいうと freee の FY2020/6 とマネーフォワードの FY/2020/11 の売上を足した数字より大きい。

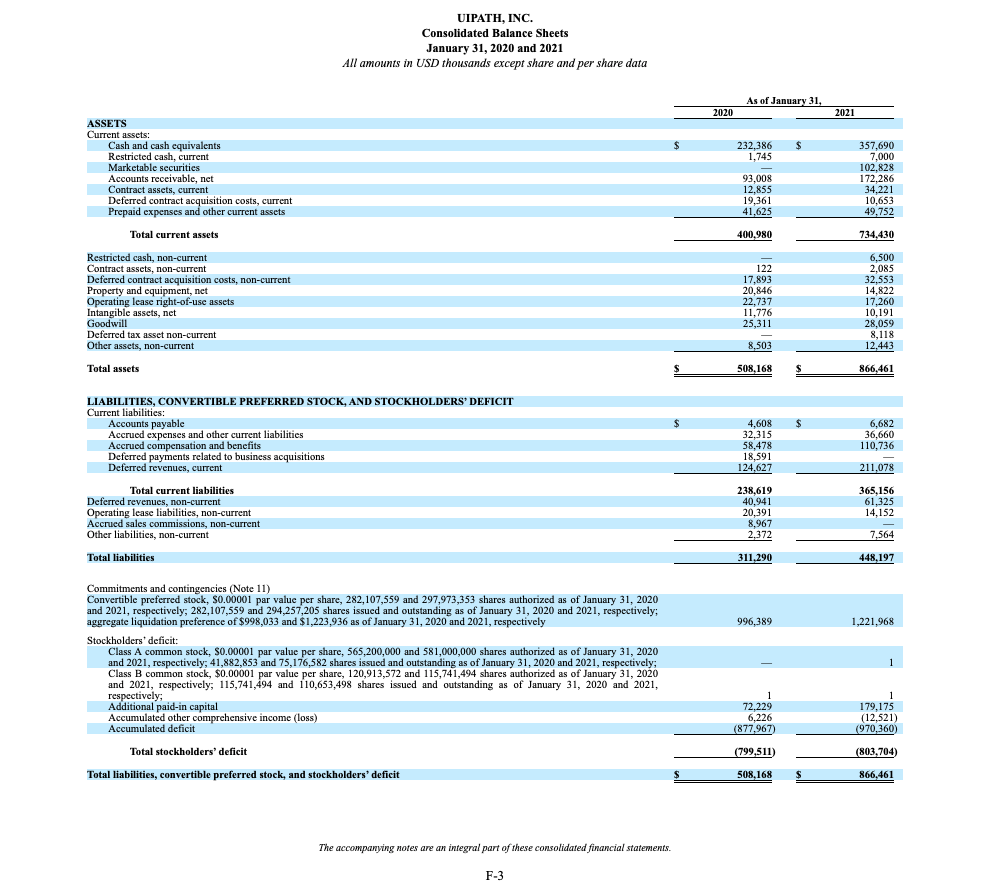

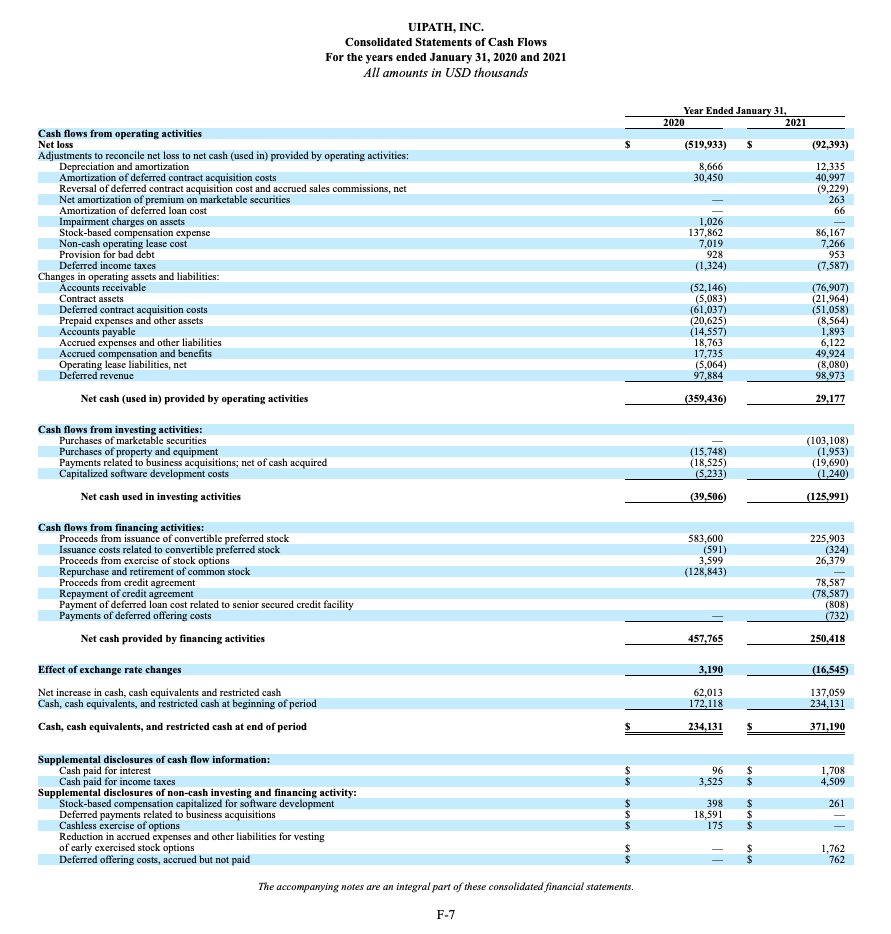

BS/PL/CF を貼っておく

さらっと読んだだけで特筆すべきことはないのだが、 BS と CF を見ると派手にお金使ってるなぁという印象がある。

FY2021 の Cash は $357,690k だが、これは FY2020 の営業 CF のマイナスと同じくらいだ。今回の IPO に加えて 2021 年 2 月に Series F で $750M の大金を調達してるのでお金はたくさんあるのだが、自分が経営者だったらこんなに派手にお金使えないと思う。

RPA に対する個人的な意見

私は RPA と呼ばれる製品やサービスに頼りすぎるのは良くないと考えている。

プログラミングせずとも様々な作業を自動化できて便利ではあるが、仕事の改善をし続けていくためにはその作業の背後にあるデータモデルやワークフローについてしっかり考えてそれを形にする必要があって、現状の RPA 製品・サービスの機能はそれらを考えなくていいほど進歩しているとは思えないからだ。

役割や限界を意識して道具として使うのはいいと思うけど、これさえあれば万事解決!というものではない。これは何にでも言えることかもしれないが…

Footnotes

-

未上場で企業価値 10 億ドル以上の企業 ↩